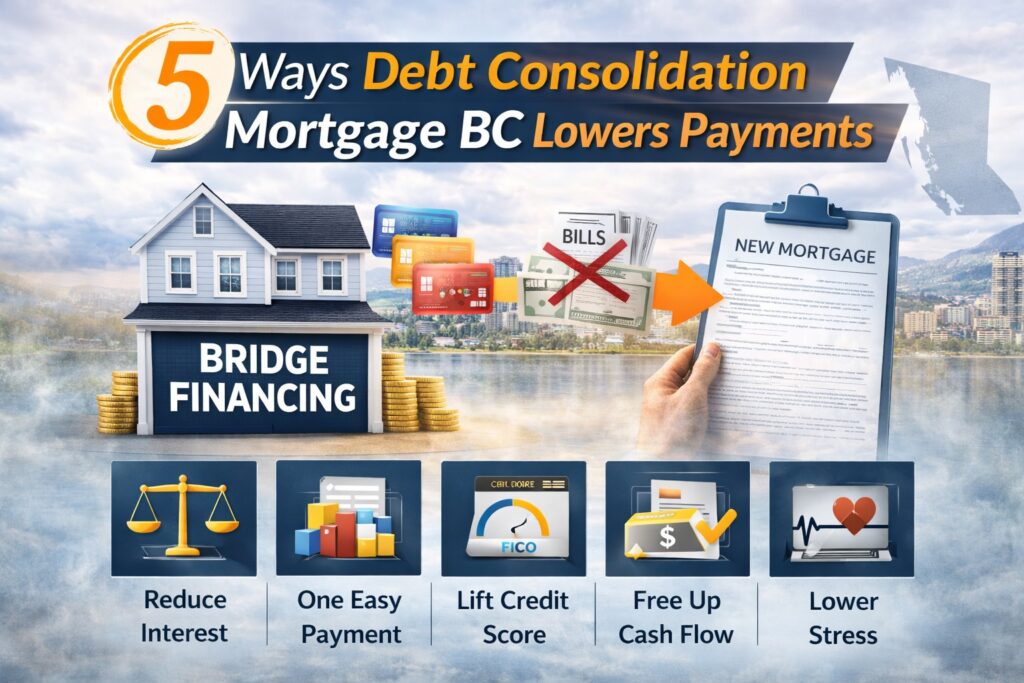

Debt Consolidation Mortgage BC: 5 Ways to Lower Your Monthly Payments

A debt consolidation mortgage in BC allows homeowners to use equity in their property to pay off high-interest consumer debt and replace multiple monthly payments with a single, lower mortgage payment. For homeowners in Surrey, Langley, and the Lower Mainland carrying credit card balances, personal loans, car payments, or lines of credit, debt consolidation mortgage BC solutions can significantly improve monthly cash flow and reduce total interest paid over time.

Understanding how debt consolidation mortgages work and when they make financial sense requires looking at the specific numbers in your situation.

Replace High Interest Debt With Lower Mortgage Rates

The primary advantage of a debt consolidation mortgage in BC is the interest rate differential. Credit cards typically charge 19 to 29 percent annual interest. Personal loans and lines of credit range from 8 to 15 percent. Car loans sit around 6 to 10 percent depending on credit profile. A debt consolidation mortgage in BC refinances these obligations at mortgage rates, which currently range from approximately 5 to 7 percent for traditional lenders and 7 to 12 percent for alternative lenders.

Even when using alternative lending for a debt consolidation mortgage in BC due to credit or income documentation challenges, the mortgage rate is almost always lower than the rates on unsecured consumer debt. This rate reduction translates directly into lower monthly payments and less total interest paid over the life of the debt.

For example, a homeowner in Surrey carrying 50,000 dollars in credit card debt at 21 percent interest pays over 1,000 dollars monthly just to cover minimum payments, with most of that going toward interest rather than principal reduction. Consolidating that debt into a mortgage at 8 percent through a debt consolidation mortgage BC refinance reduces the payment significantly while actually paying down the balance.

Combine Multiple Payments Into One Monthly Amount

Beyond interest savings, a debt consolidation mortgage in BC simplifies your financial life by replacing multiple payment due dates, amounts, and creditors with a single monthly mortgage payment. Homeowners juggling credit card payments, a car loan, a line of credit, and personal loan obligations deal with multiple due dates throughout the month, each requiring attention and planning to avoid missed payments or NSF fees.

A debt consolidation mortgage in BC eliminates this complexity. One payment date, one amount, one place to send funds. This simplification reduces the mental load of debt management and decreases the risk of accidentally missing a payment due to confusion about timing or amounts.

For homeowners in the Lower Mainland managing tight monthly budgets, this consolidation also makes cash flow planning much more straightforward. You know exactly when your mortgage payment is due and exactly how much it will be, making it easier to plan around income timing and other obligations.

Improve Credit Score By Reducing Credit Utilization

A debt consolidation mortgage in BC can improve your credit score in two important ways. First, paying off credit card balances and lines of credit through mortgage refinancing immediately reduces your credit utilization ratio, which is the percentage of available revolving credit you are currently using. Credit utilization accounts for approximately 30 percent of your credit score calculation, and high utilization drags scores down significantly.

When you use a debt consolidation mortgage in BC to pay off credit cards and lines of credit, those accounts show zero balances but remain open with their full available credit limits. This dramatically improves your utilization ratio overnight. A homeowner carrying 40,000 dollars in balances across credit cards with 50,000 dollars in total limits has 80 percent utilization, which negatively impacts their score. After debt consolidation mortgage BC refinancing pays off those balances, utilization drops to zero percent, often resulting in a credit score increase within one to two billing cycles.

Second, consolidating multiple debts into a single mortgage payment reduces the number of monthly obligations that could potentially be missed or paid late. Each missed payment damages your credit score. Simplifying to one payment through a debt consolidation mortgage in BC reduces this risk going forward.

Access Tax Deductible Interest on Investment Properties

For homeowners who own investment properties in BC, a debt consolidation mortgage can provide an additional benefit beyond lower rates and simplified payments. Interest paid on debt used to earn investment income is tax deductible in Canada. If you refinance an investment property with a debt consolidation mortgage BC and use the proceeds to pay off non-deductible consumer debt, and then use the freed-up cash flow to make investments, you may be able to restructure your debt in a tax-advantaged way.

This strategy requires proper structuring and documentation, and homeowners should consult with a tax professional to ensure compliance with Canada Revenue Agency guidelines. However, for investors carrying both consumer debt and investment properties, a debt consolidation mortgage in BC can potentially convert non-deductible interest into deductible interest when structured correctly.

Stop Collection Calls and Reduce Financial Stress

The financial benefits of a debt consolidation mortgage in BC are measurable and concrete, but the psychological and stress-reduction benefits are equally important. Homeowners dealing with overwhelming consumer debt often face collection calls, threatening letters, and the constant anxiety of not being able to keep up with minimum payments across multiple creditors.

A debt consolidation mortgage in BC immediately eliminates this pressure. All creditors are paid in full through the mortgage refinance. Collection activity stops. The multiple payment obligations disappear. The homeowner is left with a single, manageable mortgage payment and the breathing room to focus on rebuilding financial stability rather than constantly juggling payment demands.

For families in Surrey, Langley, and the Lower Mainland dealing with the stress of unmanageable debt, the emotional relief that comes with a successful debt consolidation mortgage BC refinance is often as valuable as the financial savings.

When Does Debt Consolidation Mortgage BC Make Sense?

A debt consolidation mortgage in BC is not the right solution in every situation. It works best when you have sufficient equity in your property to refinance, when the interest savings justify any costs associated with refinancing, and when you are committed to not accumulating new consumer debt after consolidation.

Homeowners who consolidate debt through mortgage refinancing but then run up new credit card balances end up in a worse position than before, with both a larger mortgage and new consumer debt. Successful debt consolidation mortgage BC strategies require a commitment to changed spending habits and financial discipline going forward.

The math also needs to work in your favor. If you are carrying low-interest debt or very small balances, the cost of refinancing may exceed the benefits. A mortgage broker can help you analyze your specific situation and determine whether a debt consolidation mortgage in BC produces meaningful savings or whether other debt management strategies would serve you better.

Alternative Lenders and Debt Consolidation Mortgage BC

Many homeowners who would benefit from a debt consolidation mortgage in BC have been declined by traditional banks. The credit damage caused by carrying high consumer debt often results in credit scores below bank thresholds. Self-employed borrowers managing debt alongside business obligations may struggle with income documentation. Other borrowers simply need to access more equity than traditional lenders allow.

Alternative lenders in BC, including B lenders and private lenders, specialize in debt consolidation mortgage scenarios where traditional banks decline. These lenders focus more heavily on property equity and less on credit score or income documentation complexity. While rates are higher than traditional bank mortgages, they are still substantially lower than credit card and consumer loan rates, making the consolidation financially beneficial.

Working with a mortgage broker who understands both traditional and alternative lending for debt consolidation mortgage BC scenarios ensures you find the best available solution for your specific situation. Mortgage brokers in BC are licensed and regulated by the Financial Services Regulatory Authority of BC, which provides consumer protection and enforces professional standards.

For additional information about mortgage lending regulations in British Columbia, visit the Financial Services Regulatory Authority of BC at fsrao.ca or review mortgage resources through the Canada Mortgage and Housing Corporation at cmhc-schl.gc.ca.

Let’s Analyze Your Debt Consolidation Mortgage BC Options

If you are carrying high-interest consumer debt and have equity in your BC property, a debt consolidation mortgage may significantly improve your financial situation. The first step is running the actual numbers to see what the savings look like in your case.

I work with debt consolidation mortgage BC scenarios regularly throughout Surrey, Langley, the Lower Mainland, and Calgary. My approach is to review your current debt obligations, calculate what consolidation would save you monthly and over time, and help you determine whether refinancing makes sense or whether other debt management strategies would serve you better.

For more information about using home equity to eliminate debt, visit https://greghorvath.ca/private-financing/

Book a consultation at greghorvath.ca. There is no cost and no obligation. Let’s look at your debt structure and see if a debt consolidation mortgage in BC is the right solution for your situation.