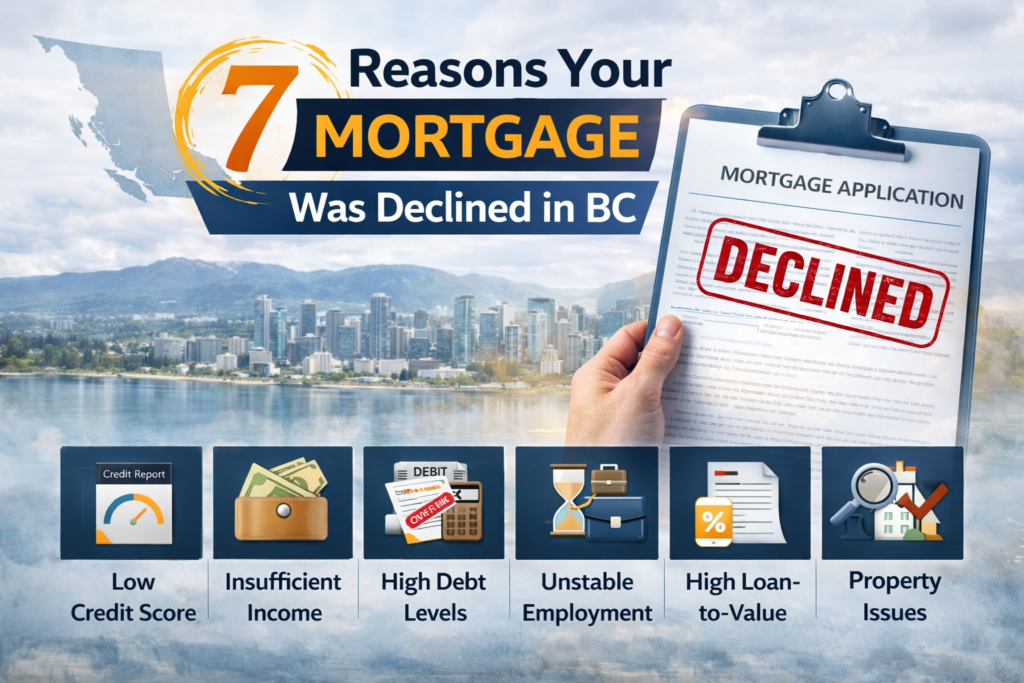

7 Reasons Your Mortgage Was Declined in BC and What to Do Next

Mortgage declined applications are frustrating, especially when you thought approval was straightforward. If your mortgage was declined in BC, understanding why the bank said no is the first step toward finding a solution. Most mortgage declines fall into a handful of common categories, and for nearly every decline reason, alternative financing options exist that can help you move forward.

Here are the seven most common reasons mortgages get declined in BC and what your options are when traditional lenders turn you down.

Insufficient Income Documentation

When a mortgage is declined in BC due to income, the issue is rarely that you do not earn enough money. The problem is almost always how that income is documented. Banks require two years of consistent, provable income reported on your Notice of Assessment from the Canada Revenue Agency. If you are self-employed, incorporated, or your income structure does not fit neatly into their underwriting boxes, banks will decline the application even if your actual earnings are strong.

Self-employed borrowers who write off business expenses, draw minimal salary to reduce taxes, or retain earnings inside a corporation frequently have their mortgage declined in BC for this reason. The income exists, but the documentation does not satisfy traditional lending criteria.

Alternative lenders in BC assess income differently. They may use bank statement analysis to review actual cash flow, consider gross business revenue, or offer stated income programs where you declare your earnings and the lender applies reasonability testing based on your industry and business type. These approaches allow many borrowers whose mortgage was declined in BC due to income documentation to secure financing.

Credit Score Below Bank Thresholds

Most traditional lenders in BC require a minimum credit score of 600 to 650 for mortgage approval, with better rates available to borrowers above 680. If your mortgage was declined in BC because your credit score falls below these thresholds, you are not out of options.

Credit scores can drop for many reasons that do not reflect your current financial stability. A consumer proposal, past bankruptcy, missed payments during a period of financial difficulty, or simply limited credit history can all result in a score that causes banks to decline your mortgage application in BC.

B lenders and private lenders in British Columbia work with borrowers across a much wider credit spectrum. B lenders typically accept scores as low as 550 to 600, while private lenders focus primarily on equity in the property rather than credit score. If your mortgage was declined in BC due to credit, these lenders provide a path forward while you work on rebuilding your score over time.

High Debt Service Ratios

Banks calculate two key ratios when assessing mortgage applications: Gross Debt Service ratio and Total Debt Service ratio. These ratios measure how much of your income goes toward housing costs and total debt payments. If your mortgage was declined in BC because these ratios exceed bank maximums, the lender has determined that adding a mortgage payment would stretch your budget too thin based on their guidelines.

This decline reason is common among borrowers with significant consumer debt, car loans, or other ongoing payment obligations. Even if your income is strong, high debt service ratios can trigger a mortgage decline in BC.

Alternative lenders apply more flexible debt service calculations and may be willing to work with higher ratios if other compensating factors exist, such as strong equity, clean payment history on existing debts, or documented plans to consolidate and pay down obligations after the mortgage funds.

Insufficient Down Payment or Equity

If your mortgage was declined in BC due to insufficient down payment, the bank has determined that your equity position does not meet their requirements. For purchases, this typically means you need to increase your down payment. For refinances, it means the amount you want to borrow exceeds the lender’s maximum loan-to-value ratio based on your property’s appraised value.

Traditional lenders in BC generally cap refinances at 80 percent loan-to-value, meaning you need at least 20 percent equity remaining in your home after the new mortgage funds. If you are looking to access more equity than this, banks will decline the application.

Private lenders in BC often lend up to higher loan-to-value ratios, sometimes reaching 85 percent depending on property type and location. If your mortgage was declined in BC because you need to access more equity than traditional lenders allow, private financing can bridge that gap in the short term.

Property Does Not Meet Lending Criteria

Sometimes a mortgage is declined in BC not because of your financial profile, but because of the property itself. Banks have strict property criteria and will decline mortgages on properties they consider higher risk or difficult to resell.

Common property-related decline reasons include rural or remote locations, properties requiring significant repairs, unique or unconventional homes, properties on leased land, or homes in markets the lender considers unstable. If your mortgage was declined in BC for property-related reasons, the issue has nothing to do with your qualifications as a borrower.

Private lenders evaluate properties individually and are often more flexible about property type and condition, provided the underlying value supports the loan. If your mortgage was declined in BC due to property characteristics, private financing may be the solution that allows the transaction to proceed.

Recent Credit Events

If your mortgage was declined in BC due to a recent bankruptcy, consumer proposal, foreclosure, or other significant credit event, banks typically impose waiting periods before they will consider your application. These waiting periods can range from two to seven years depending on the event and the lender’s specific policies.

While you wait for these timelines to pass, life does not stop. You may need to purchase a home, refinance to consolidate debt, or access equity for other important financial goals. Alternative lenders in BC do not impose the same rigid waiting periods and will assess your current financial situation rather than focusing exclusively on past credit events.

If your mortgage was declined in BC because a credit event is still within the bank’s exclusion period, alternative lending provides a pathway to securing financing now rather than waiting years for traditional approval.

Employment or Income Stability Concerns

Banks want to see stable, predictable income from a consistent source. If your mortgage was declined in BC because you recently changed jobs, started a new business, work on contract or commission, or have gaps in your employment history, the lender has determined your income does not meet their stability requirements.

This decline reason is common among borrowers whose income is actually strong and reliable but structured in ways that do not fit traditional lending templates. Contract workers, commissioned sales professionals, seasonal workers, and entrepreneurs often have their mortgage declined in BC despite earning well above the income needed to support the payments.

Alternative lenders assess income stability differently and place more weight on your actual track record of managing financial obligations than on rigid employment criteria. If your mortgage was declined in BC due to employment or income structure concerns, alternative financing options exist that evaluate your situation more holistically.

What to Do When Your Mortgage Is Declined in BC

If your mortgage was declined in BC, the first step is understanding exactly why the decline happened. Request a clear explanation from the lender so you know which specific issue triggered the decision. Once you understand the reason, you can evaluate your options.

For many decline reasons, alternative lenders in British Columbia provide viable solutions. B lenders offer a middle ground between banks and private lenders, with more flexible criteria than traditional institutions but lower rates than private financing. Private lenders focus primarily on equity and property value, making them ideal for situations where income documentation, credit, or employment concerns caused the bank decline.

Working with a mortgage broker who specializes in alternative lending ensures you understand all available options and helps match your situation to the right lender. Mortgage brokers in BC are licensed and regulated by the Financial Services Regulatory Authority of BC, which enforces professional standards and consumer protection.

For additional information about mortgage regulations in British Columbia, visit the Financial Services Regulatory Authority of BC at fsrao.ca or review mortgage resources through the Canada Mortgage and Housing Corporation at cmhc-schl.gc.ca.

Let’s Find Your Solution After a Mortgage Decline in BC

If your mortgage was declined in BC, that decline is not a final answer. It simply means that particular lender’s criteria did not align with your file. Alternative financing options exist for nearly every decline scenario.

I work with mortgage decline situations regularly throughout Surrey, Langley, the Lower Mainland, and Calgary. My approach is to understand exactly why your mortgage was declined in BC, explain what your options are, and help you make a decision that moves you forward.

For more information about alternative mortgage solutions, visit https://greghorvath.ca/private-financing/

Book a consultation at greghorvath.ca. There is no cost and no obligation. Let’s review what happened with your decline and what your next steps should be.