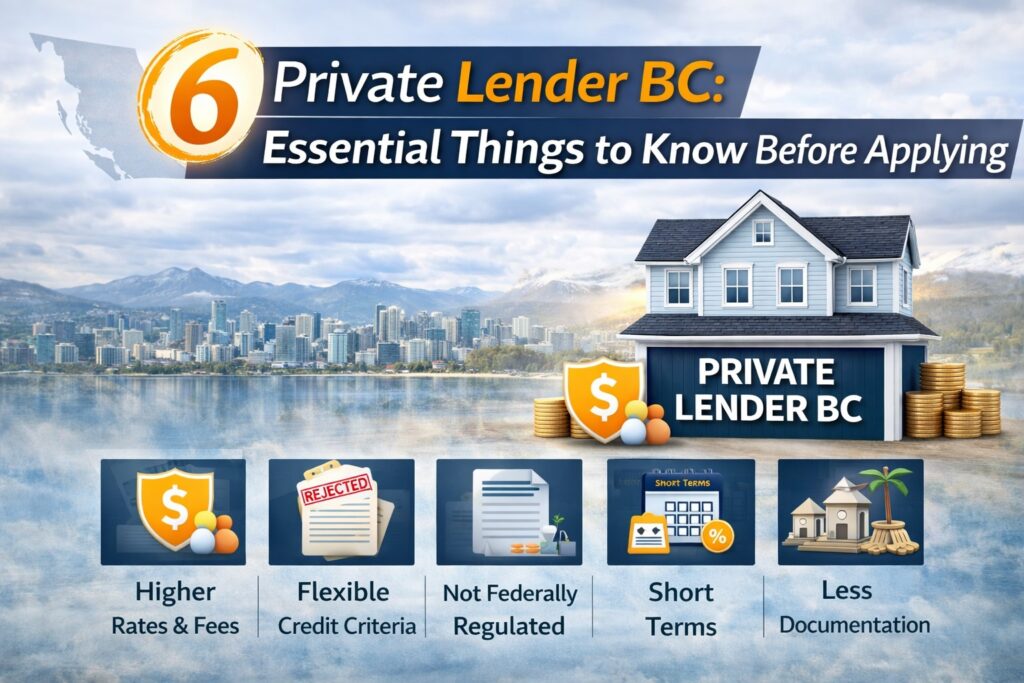

Private Lender BC: 6 Essential Things to Know Before You Apply

Working with a private lender in BC opens financing options when traditional banks and credit unions decline your mortgage application. Private lenders operate differently from institutional lenders, focusing primarily on property equity rather than credit scores or income documentation. For borrowers across Surrey, Langley, and the Lower Mainland who do not fit traditional lending criteria, private lender BC solutions provide access to capital that would otherwise be unavailable.

Understanding how private lenders work, what they cost, and what to expect from the process helps you make informed decisions when traditional financing is not an option.

Private Lender BC Approval Focuses on Equity Not Credit

The fundamental difference between a private lender in BC and a traditional bank is what drives the approval decision. Banks assess your income, employment stability, credit score, and debt ratios to determine whether you can afford the mortgage payments. Private lenders in BC assess the equity in your property and the loan-to-value ratio to determine whether the deal makes sense from a security perspective.

A private lender in BC typically approves mortgages up to 75 to 80 percent of the property’s appraised value, sometimes higher in strong real estate markets like Vancouver, Burnaby, Surrey, and Langley. This means if your home is worth one million dollars, a private lender in BC may lend up to 750,000 to 800,000 dollars regardless of your credit score or employment situation, as long as sufficient equity exists to secure the loan.

This equity-focused approach means borrowers who have been declined by banks due to credit challenges, self-employment income documentation issues, recent bankruptcy or consumer proposal, or non-traditional income sources can often secure financing through a private lender in BC if they have built equity in their property.

Interest Rates From Private Lender BC Are Higher

Private lender BC interest rates range from approximately 8 to 12 percent depending on the specific deal, loan-to-value ratio, property type and location, and overall risk profile. These rates are significantly higher than traditional bank mortgage rates, which currently range from 5 to 7 percent for qualified borrowers.

The higher rates from a private lender in BC reflect the increased risk these lenders take by approving borrowers who do not meet traditional lending criteria. While the rates are higher than bank mortgages, they are typically lower than credit card rates, personal loan rates, and other forms of unsecured consumer debt.

Most borrowers who work with a private lender in BC use these mortgages as short-term solutions rather than long-term financing. The typical approach is to use a private lender in BC to access needed capital immediately, then work to improve credit, income documentation, or equity position over the next one to two years before refinancing into lower-cost traditional or B lender financing.

Lender Fees and Broker Fees Apply to Private Lender BC Mortgages

In addition to interest, private lender BC mortgages involve upfront fees that borrowers need to understand before proceeding. Private lenders charge lender fees, also called arrangement fees or commitment fees, typically ranging from 1 to 3 percent of the mortgage amount. These fees compensate the lender for underwriting and funding the mortgage.

Mortgage brokers who arrange financing through a private lender in BC also charge broker fees, typically 1 to 2 percent of the mortgage amount. These fees compensate the broker for sourcing the deal, presenting it to the lender, and managing the approval and funding process.

Combined, lender and broker fees for a private lender BC mortgage typically total 2 to 5 percent of the loan amount. On a 500,000 dollar private mortgage, this means 10,000 to 25,000 dollars in upfront fees in addition to the ongoing interest charges. These fees are disclosed upfront and are typically deducted from the mortgage proceeds at funding rather than paid separately.

While these fees add to the overall cost of using a private lender in BC, they provide access to capital that would not otherwise be available. The key is ensuring the total cost justifies the benefit you receive from the financing.

Private Lender BC Terms Are Typically One to Two Years

Most private lender BC mortgages are structured with terms of one to two years rather than the five-year terms common with traditional mortgages. This short-term structure aligns with how most borrowers use private financing as a temporary bridge to traditional lending.

At the end of the term, borrowers typically have three options. They can refinance with a traditional lender or B lender if their situation has improved, renew the private mortgage for another term if they still need more time to qualify elsewhere, or sell the property and repay the private lender in full from the proceeds.

The short term means borrowers need a realistic exit strategy before working with a private lender in BC. Simply hoping your situation will improve without taking concrete steps to address the issues that led you to private lending in the first place often results in being stuck in expensive financing longer than necessary.

Exit Strategy Matters When Working With Private Lender BC

A strong exit strategy is critical when you work with a private lender in BC. The lender wants to understand how you plan to repay or refinance the mortgage before the term expires. Common exit strategies include selling the property before term maturity, refinancing to a traditional or B lender once credit is repaired or income is better documented, paying down the mortgage through business income or other sources until loan-to-value drops enough for traditional refinancing, or receiving proceeds from an expected event like an inheritance or business sale.

Borrowers without a clear and realistic exit strategy may find themselves trapped in expensive private financing or forced to sell their property under pressure when the term matures. Working with an experienced mortgage broker who helps you develop a viable exit plan before approaching a private lender in BC ensures you enter the arrangement with a path forward rather than simply kicking the can down the road.

Not All Private Lender BC Options Are Equal

The private lending market in BC includes both reputable, professional lenders who operate transparently and predatory lenders who take advantage of desperate borrowers. The difference between working with a quality private lender in BC and a predatory one can have serious financial consequences.

Quality private lenders in BC charge market rates and fees, disclose all costs upfront, fund deals in reasonable timeframes, and work professionally with brokers and borrowers. Predatory lenders charge excessive fees, add hidden costs not disclosed upfront, make funding contingent on additional payments or requirements not part of the original agreement, or engage in other practices that exploit borrowers in difficult situations.

Working with a licensed mortgage broker who has established relationships with reputable private lenders in BC protects you from predatory lending practices. Mortgage brokers in British Columbia are licensed and regulated by the Financial Services Regulatory Authority of BC, which enforces professional standards and consumer protection.

For additional information about mortgage lending regulations in British Columbia, visit the Financial Services Regulatory Authority of BC at fsrao.ca or review mortgage resources through the Canada Mortgage and Housing Corporation at cmhc-schl.gc.ca.

When Does Working With Private Lender BC Make Sense?

Private lender BC mortgages make sense when you have been declined by traditional lenders but have sufficient equity in your property, when you need to close on a purchase or refinance quickly and cannot wait for traditional approval timelines, when you are navigating a short-term financial challenge and need a bridge to better financing, or when traditional lenders will not finance your property type or situation but the deal has merit.

Private lending does not make sense when you have no realistic path to refinancing or repaying before term maturity, when the total cost of private financing exceeds the benefit you receive, when you could qualify for traditional or B lender financing with minor adjustments to your application, or when the financing is enabling spending or lifestyle choices that are not sustainable.

An experienced mortgage broker can help you evaluate whether working with a private lender in BC is the right solution for your specific situation or whether other options would serve you better.

Let’s Discuss Your Private Lender BC Options

If you have been declined by traditional lenders and are considering working with a private lender in BC, understanding your full range of options and ensuring you work with reputable lenders at fair market rates is critical.

I work with private lender BC scenarios regularly throughout Surrey, Langley, the Lower Mainland, and Calgary. My approach is to explain how private lending works, what it will cost in your specific situation, help you develop a realistic exit strategy, and ensure you work with quality lenders who operate professionally and transparently.

For more information about private lending solutions, visit https://greghorvath.ca/private-financing/

Book a consultation at greghorvath.ca. There is no cost and no obligation. Let’s review whether a private lender in BC is the right solution for your situation and ensure you enter any arrangement with full information and realistic expectations.