How to Refinance Your Mortgage BC When Banks Say No: 6 Alternative Options

When you need to refinance mortgage BC and traditional banks decline your application, understanding your alternative options becomes critical. Homeowners across Surrey, Langley, and the Lower Mainland refinance for many valid reasons including accessing equity for renovations, consolidating debt, funding business investments, or simply securing better terms. When traditional lenders say no, alternative refinancing solutions exist that focus less on perfect credit and income documentation and more on the equity you have built in your property.

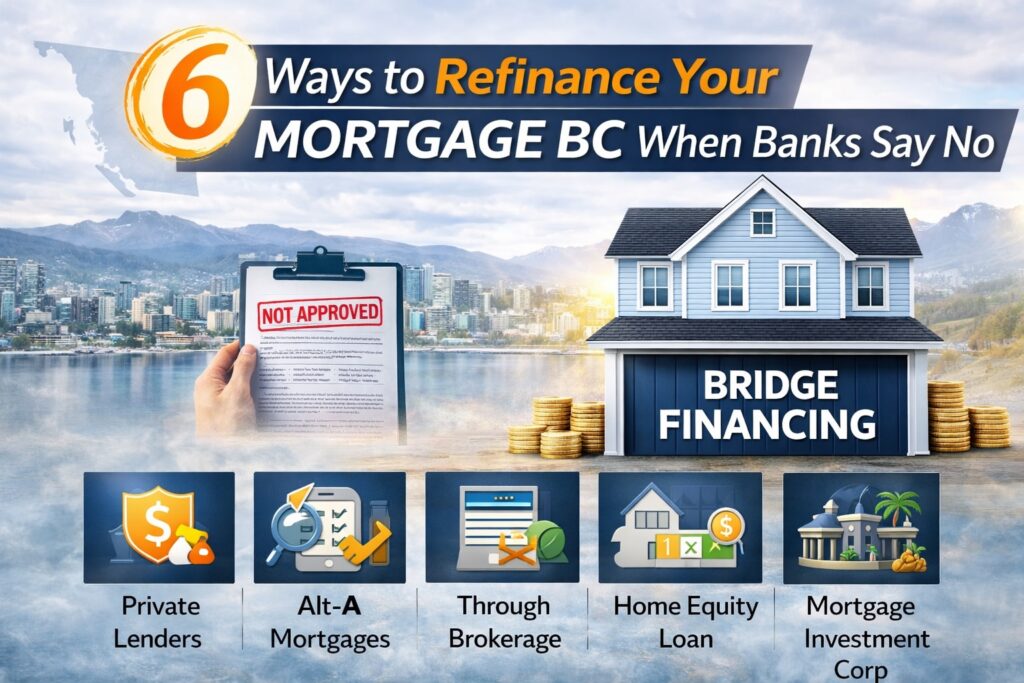

Here are six ways to successfully refinance mortgage BC when banks decline your application.

Work With B Lenders for Refinance Mortgage BC Approval

B lenders occupy the middle ground between traditional banks and private lenders when you need to refinance mortgage BC. These lenders are regulated financial institutions that accept applications from borrowers who do not fit standard bank criteria but still maintain reasonable credit and financial profiles.

B lenders will refinance mortgage BC for borrowers with credit scores as low as 550 to 600, recent credit events like consumer proposals or past bankruptcies, non-traditional income sources, or self-employment without perfect tax documentation. Interest rates from B lenders are typically 1 to 3 percent higher than traditional bank rates, which is significantly less expensive than private lending while still providing access to refinancing when banks decline.

For homeowners who need to refinance mortgage BC but have experienced credit challenges or income documentation issues, B lenders often provide the best balance of accessible approval criteria and reasonable costs. These lenders can refinance up to 80 to 85 percent loan-to-value in many cases, allowing you to access substantial equity even with credit or income concerns.

Use Private Lenders to Refinance Mortgage BC Based on Equity

Private lenders focus primarily on equity when you need to refinance mortgage BC. If you have been declined by banks and B lenders, or if you need to access equity quickly without waiting for traditional approval timelines, private mortgage refinancing provides a solution.

Private lenders in BC will refinance mortgage based on the loan-to-value ratio rather than credit score or income documentation. As long as you have sufficient equity in your property and the deal makes sense from a security perspective, private lenders can approve and fund refinancing in days rather than weeks.

Interest rates for private mortgage refinancing in BC range from approximately 8 to 12 percent depending on the deal structure and risk profile. While higher than traditional rates, private refinancing allows you to access equity when no other options exist. Many homeowners use private refinancing as a short-term bridge, accessing needed funds immediately while working to improve credit or income documentation to refinance into lower-cost options later.

Private lenders can often refinance mortgage BC up to 75 to 80 percent loan-to-value, and in some cases higher depending on property location and type. For homeowners in strong real estate markets like Vancouver, Surrey, Burnaby, and Langley, this can mean access to substantial equity even when traditional lenders decline.

Consider Home Equity Lines of Credit as Refinance Mortgage BC Alternatives

If your goal when you refinance mortgage BC is to access equity for ongoing expenses, renovations, or business investments rather than a one-time lump sum, a home equity line of credit may serve you better than traditional refinancing.

HELOCs provide revolving credit secured against your property equity, allowing you to draw funds as needed up to your approved limit and pay interest only on the amount actually borrowed. Alternative lenders in BC offer HELOCs to borrowers who do not qualify with traditional banks, using equity-focused underwriting similar to private mortgage refinancing.

The advantage of a HELOC when you need to refinance mortgage BC for flexible access to funds is that you pay interest only on what you use, potentially saving significant money compared to refinancing your entire mortgage balance at a higher rate just to access equity. HELOCs from alternative lenders in BC typically carry interest rates in the 7 to 10 percent range, positioning them between B lender mortgages and private mortgages in terms of cost.

Explore Second Mortgages to Refinance Mortgage BC Without Touching Your First

If you currently have a favorable interest rate on your existing first mortgage and do not want to break it to refinance mortgage BC at a higher rate, a second mortgage allows you to access equity while leaving your first mortgage untouched.

Second mortgages sit in second position behind your existing mortgage and allow you to borrow against available equity without refinancing your entire mortgage balance. This strategy makes particular sense when interest rates have risen since you obtained your original mortgage or when breaking your current mortgage would trigger substantial prepayment penalties.

Alternative lenders and private lenders in BC offer second mortgages to homeowners who would not qualify to refinance mortgage BC through traditional channels. Second mortgage rates are higher than first mortgage rates due to the increased lender risk of being in second position, typically ranging from 9 to 14 percent depending on your equity position and the lender used.

The combined payments on your first and second mortgages need to fit within your budget, but for many homeowners, a second mortgage provides the most cost-effective way to refinance mortgage BC and access needed equity without disturbing favorable existing financing.

Wait Until Mortgage Renewal to Refinance Mortgage BC

If your mortgage term is approaching maturity and you need to refinance mortgage BC but current lenders are declining you, waiting until your renewal date eliminates prepayment penalties and may open additional options.

At mortgage renewal, you are not locked into staying with your existing lender. You can shop the market, including alternative lenders, without penalty. While you still need to qualify based on current lending criteria, the absence of breakage costs makes it easier to move to an alternative lender who will approve your refinance mortgage BC application even if your existing lender will not.

If your renewal is more than six months away, working with a mortgage broker to line up alternative financing in advance ensures you have options ready when your term matures. This advance planning prevents being forced into whatever terms your existing lender offers simply because you did not arrange alternatives before renewal.

Improve Your Refinancing Profile Before Reapplying to Refinance Mortgage BC

If you do not need to refinance mortgage BC immediately, taking time to strengthen your application can open doors to better rates and terms when you do proceed with refinancing.

Common improvements that increase refinance mortgage BC approval odds include paying down consumer debt to improve debt service ratios, correcting errors on credit reports and building credit score through consistent on-time payments, allowing time to pass after credit events like bankruptcy or consumer proposal, improving income documentation for self-employed borrowers by adjusting how income is drawn or reported, and building additional equity through property value appreciation or mortgage paydown.

While these improvements take time, the savings from qualifying for B lender rates instead of private rates can be substantial. If your timeline allows, strengthening your profile before you refinance mortgage BC may save thousands of dollars over the term of your refinancing.

Working With a Broker to Refinance Mortgage BC

When you need to refinance mortgage BC and traditional lenders decline your application, working with a mortgage broker who specializes in alternative lending ensures you understand all available options and find the most cost-effective solution for your situation.

Mortgage brokers in BC have access to multiple B lenders and private lenders, can compare rates and terms across the market, understand which lenders work best for specific refinance scenarios, and can often secure better rates than going directly to lenders. Brokers are licensed and regulated by the Financial Services Regulatory Authority of BC, which enforces professional standards and consumer protection.

For additional information about mortgage lending regulations in British Columbia, visit the Financial Services Regulatory Authority of BC at fsrao.ca or review mortgage resources through the Canada Mortgage and Housing Corporation at cmhc-schl.gc.ca.

Let’s Find Your Path to Refinance Mortgage BC

If you have been declined by traditional lenders when trying to refinance mortgage BC, alternative options exist. Whether through B lenders, private lenders, second mortgages, or HELOCs, there is almost always a path to accessing your equity if the numbers make sense.

I work with refinance mortgage BC scenarios regularly throughout Surrey, Langley, the Lower Mainland, and Calgary. My approach is to understand why traditional lenders declined you, explain what alternative options are available, and help you choose the solution that balances accessibility with cost-effectiveness.

For more information about alternative refinancing solutions, visit https://greghorvath.ca/private-financing/

Book a consultation at greghorvath.ca. There is no cost and no obligation. Let’s review your refinance needs and find the best available solution when banks say no.